Buying a business can be one of the fastest ways to become an entrepreneur, but it’s also one of the riskiest if you miss critical warning signs early. According to industry research, more than 70% of failed mergers and acquisitions trace back to insufficient due diligence or overlooked red flags, issues that could have been spotted with a rigorous review process.

The most common red flags fall into a few deal-critical areas. Unreliable or missing financials undermine valuation and cash-flow confidence. Hidden liabilities, including undisclosed debt or off-book obligations, can drain cash after closing. Customer or supplier concentration increases the risk of sudden revenue or operational loss. Owner-dependent or undocumented operations weaken transferability. People and culture issues, such as high turnover or weak management depth, often surface once the seller exits. Outdated systems and unresolved legal, tax, or IP issues quietly erode earnings and raise post-close risk. These signals determine whether a buyer should walk away, reprice, or add protections through diligence and deal structure.

Detecting hidden problems before closing prevents costly surprises after the sale. Poor acquisitions lead to "no end of headaches”, from legal exposure to sudden customer loss. Due diligence exists to reveal liabilities that don't show up in headline earnings.

Hidden issues convert into real post-close costs: legal claims, tax penalties, equipment failures, lost clients, and key employee departures. Each cost reduces net value and can force unexpected capital injections.

In practice, spotting issues changes price, timing, and support needs. A buyer may lower the offer, split payments over time, or require seller transition help to protect value.

Opportunity cost matters. Spending time on a flawed purchase pulls focus from better targets. Trust your gut, but always validate with documents and independent verification. Elite Exit Advisors recommends combining clear checklists and third-party reviews to keep emotions in check and protect your investment.

Start due diligence early to turn claims into verified facts and save time later. Knowing what buyers look for when buying a business, such as reliable financials, stable cash flow, solid operations, and manageable risks, helps focus the process. A clear document request and targeted verification reduce surprises and give lenders, buyers, and advisors a true picture of the business’s health.

Ask for an early core set of records to build a reliable picture.

Don’t rely on spreadsheets alone. Reconcile statements to bank deposits and cash collection to confirm revenue.

Use third-party appraisals for equipment and real estate. Arrange customer reference calls, ideally supervised by the seller, and confirm key vendor balances.

Operational checks matter: visit sites, observe workflow, review maintenance logs, and verify that inventory is saleable and properly valued.

Check U.S.-based reputation sources: online reviews, complaints, and complaint patterns often reveal retention risk even when topline figures look steady.

Diligence is iterative. A spike in AR or an odd lease term raises questions in other areas. Follow the trail of information until answers are complete.

.webp)

Test whether reported numbers hold up under basic verification. Missing or inconsistent financial statements often signal weak controls or deliberate concealment. That elevates risk and can be grounds to walk away.

Incomplete ledgers or tax filings hide real earnings and liabilities. Ask for reconciled P&Ls, trial balances, and tax returns. If documents are absent or contradict bank activity, treat the deal as higher risk.

Look for recurring negative operating cash flow or constant use of credit lines to cover payroll or vendor payments. Frequent overdrafts and heavy credit utilization for routine payments often mean operational stress.

High leverage diverts cash to service debts and limits reinvestment. Compare debt ratios and DSCR to industry norms; a DSCR below ~1.25 is a clear warning. Debt can strangle growth and amplify downside from a revenue dip.

Multi-year declines, seasonal weakness, shrinking average ticket size, or churn masked by discounts require scrutiny. Trending revenue down across product lines reduces valuation and raises recovery risk.

Big AR spikes may mean collection problems. Inventory surges can indicate obsolete stock or channel stuffing. Margin volatility may hide unrecorded costs or irregular pricing practices. Investigate each variance by product or customer.

Earnings quality measures how much reported profit becomes repeatable cash after owner changes and normal costs. High-quality earnings reflect sustainable performance. Low-quality earnings rely on timing or one-offs that disappear after a sale.

Rapid sales growth with swelling receivables or delayed cash suggests recognition timing tricks. Verify invoices clear to bank deposits and confirm cancellation or refund patterns in contracts.

“One-time” addbacks often include personal expenses, recurring consulting fees, or optimistic normalizations. Require documentation for every adjustment and test whether costs recur under new ownership.

Watch for overvalued inventory, low reserves, deferred maintenance, or stretched depreciation. These distort statements and mask true obligations.

Hidden obligations can suddenly change the economics of a purchase. Look beyond headline financials for liens, undisclosed loans, equipment obligations, lease guarantees, warranty exposure, and contingent claims that may surface after closing.

Some commitments live outside the balance sheet but act like debt. Temporary vendor credits, informal owner loans, or guarantees on leases can create ongoing outflows.

Watch for unusual expense patterns or vendor balances that don’t reconcile to bank records. Those inconsistencies often hint at off-record obligations.

Review AP aging for stretched terms, constant late payments, or frequent disputes. Consistent delays can mask cash shortages or strained supplier relationships.

Checks to include in the closing process: UCC searches, payoff letters, lender statements, and written confirmation that any debt tied to the company will be settled at closing.

Hidden obligations affect negotiation and increase transaction risk. Use thorough diligence, strong representations and warranties, and clear schedules of all obligations to protect the buyer and the deal.

Concentration of revenue in one or two clients can turn steady cash flow into sudden instability. Losing a major customer may create an immediate cash shortfall that breaks debt covenants or forces emergency financing.

Customer concentration thresholds to watch:

Single-source parts, long lead times, or suppliers tied personally to the owner can halt production quickly. Identify substitutes, lead-time buffers, and supplier diversification needs.

Review renewal dates, termination rights, pricing escalators, exclusivity, and change-of-control clauses that allow counterparties to exit after an acquisition.

Verification and deal response:

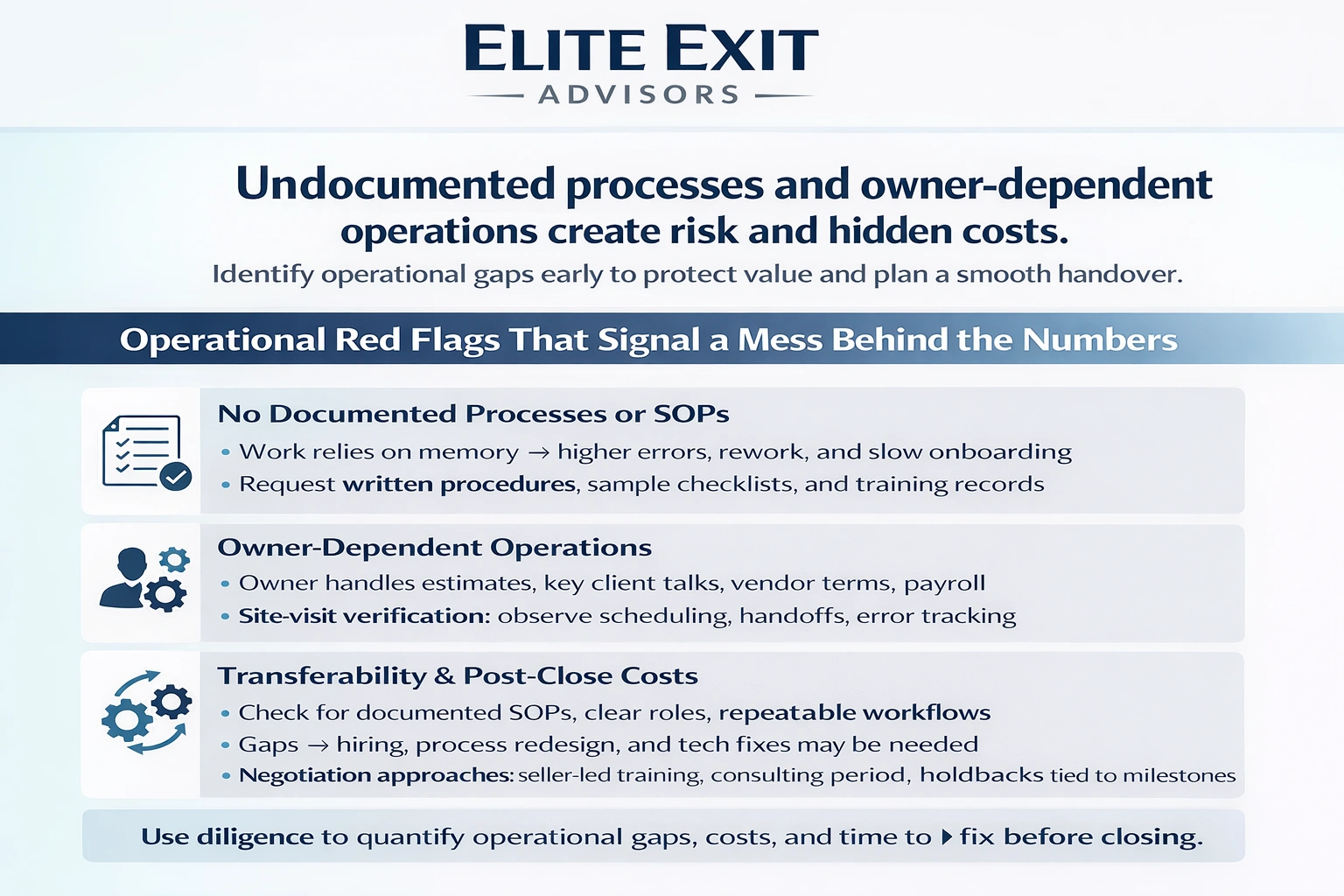

Processes that live in people’s heads create fragile operations and surprise costs after close. Undocumented procedures often mean inconsistent service, uneven quality control, and training that doesn’t scale.

When SOPs are missing, work relies on memory. That raises error rates and rework. It also makes onboarding slow and puts customer experience at risk.

Verification: request written procedures, sample job checklists, and recent training records.

Signals of owner dependence include the owner handling all estimates, key client talks, vendor terms, or payroll sign-off with no backup. That usually means the operation is not transferable without time and cost.

Negotiation approaches include seller-led training, an extended consulting period, or holdbacks linked to handover milestones. Use diligence to quantify time and cost to fix operational problems before you close.

High staff churn often signals deeper problems that will surface after closing. Turnover is an early indicator of leadership, compensation alignment, workload, training, and culture health.

Frequent departures can point to instability, low morale, scheduling issues, unresolved conflict, or reputational trouble that hurts recruiting.

Employees often leave before problems worsen. That loss increases recruitment costs and disrupts service quality.

If managers lack experience or there is no second-in-command, the buyer inherits daily firefighting and loses strategic bandwidth.

Check for cross-trained supervisors and documented role responsibilities before closing.

Changes to policies, incentives, or accountability can trigger more resignations and degrade customer experience.

Plan for cultural alignment during transition to reduce disruption.

Legacy IT can turn routine tasks into manual chores that drain time and hide true costs. In an acquisition context, technology debt is the future bill for modernization. Buyers should expect that upgrades affect valuation, CapEx planning, and the integration timeline.

Look for heavy spreadsheet use, disconnected tools, and repeated data entry. These create errors and inconsistent KPIs.

Poor reporting raises valuation and forecasting issues: unreliable numbers make cash-flow and staffing projections guesses rather than plans.

Legacy software often lacks current patches, strong access controls, or proper backups. That increases operational and regulatory risk for the company after close.

Check incident history, user permissions, and how sensitive information is stored and transmitted.

Practical diligence, an IT review, vendor inventory, and realistic upgrade budget, lets buyers quantify tech risk and plan post-close improvements. Elite Exit Advisors recommends treating systems as a core due-diligence item, not an afterthought.

Lawsuits, audits, and unclear intellectual property rights can turn an otherwise solid transaction into a costly distraction. In the U.S. context, legal or tax problems often survive closing depending on structure and contract language.

Request a schedule of current and past claims, demand letters, and regulatory correspondence. Review settlement history and assess likely exposure.

Verbal assurances are not sufficient. Treat unresolved disputes as a potential contingency that may require escrow or indemnity.

Unpaid tax liabilities, late returns, and active audits can create penalties and successor risk. Payroll tax errors are especially dangerous for buyers and lenders.

Ask for tax returns, payroll filings, and IRS or state notices. Quantify exposure and require clear payoff instructions or escrowed funds.

Confirm assignments, license scopes, trademark registrations, and renewal status. Missing deeds or signed assignments are common problems that reduce value.

Test whether key IP is protected where the company operates and whether third-party code or vendor licenses limit transferability.

Documented records should drive decisions, not verbal reassurances. Treat missing or unclear files as a red flag and require resolution before the deal moves forward.

Market shifts and local demographics often decide whether an industry can still support growth. Evaluate national trends, state migration, and consumer habit changes to see if current demand is durable.

Check industry reports, regional sales trends, and population movement. A shrinking customer base or price compression suggests limited potential.

Be conservative with forecasts in mature sectors. Use public data and trade research to stress-test seller projections.

If nearby competitors are expanding while the target is stagnant, investigate why. Losing share often signals service, price, or product gaps.

Assess whether the company truly differentiates itself or competes only on price. Lack of differentiation reduces long-term margins.

Map zoning boundaries, permit dependencies, and licensing rules that affect operations and expansion. Permit denials or restrictive zoning can halt plans.

Do independent research. Public data, local checks, and third-party reports validate seller narratives. Tie findings to valuation and contract protections to limit downside.

Valuation numbers can look solid on paper but fall apart once supporting evidence is requested. Always demand documentation that ties profit claims to bank deposits, contracts, and independent appraisals.

Inflated figures often come from aggressive addbacks, optimistic forecasts without contracts, or asset values that clash with appraisals. Verify SDE adjustments and require third-party checks to confirm true value.

Urgency or guarded document access may hide problems. Inconsistent answers, shifting reasons for sale, or missing records are warning signs that the deal needs more verification.

Watch for expiring leases with steep resets, pass-through costs, or vendors raising fees after transfer. Equipment near end-of-life, absent maintenance logs, or hard-to-source parts can create major time and replacement costs.

Confirm counts, inspect sample items, and review valuation methods. Unsellable stock can artificially boost price and create disposal costs after the sale.

Negotiation levers: price adjustments, working-capital targets, seller credits for CapEx, and conditional closing on key renewals.

Coordinated reviews across finance, operations, market, and legal reduce unseen exposure during acquisition. This approach makes verification efficient and keeps costly surprises out of scope.

Elite Exit Advisors acts as your risk-reduction partner across the full acquisition lifecycle. Our team leads early screening, organises due diligence, confirms valuation inputs, and supports negotiation strategy.

Have questions? Book a call to review a target, surface key issues, and set the next-step diligence priorities for a business acquisition. Our goal is clear: help you proceed with protection or exit before commitment becomes irreversible.

Close with a practical checklist that turns suspicion into measurable steps before you commit. Summarize the biggest red flags buying a target: verify financial statements and cash flow first, then surface hidden liabilities, and confirm customer and supplier stability plus operational transferability.

Not every issue kills the deal. Each problem must be quantified and priced into valuation, terms, or remediation. Treat reluctance to share records or pressure to rush as a cue to slow down and demand verification.

Adopt a forward-looking buyer mindset: use disciplined process, independent verification, and clear downside protection to make confident acquisition choices.